Buying a home in Portugal often becomes more realistic once you understand how much you can borrow and what the bank will expect from you. The dream may be a townhouse in Tavira, an apartment in Lisbon or a villa near Lagos, but the practical question is the same: can you finance it safely?

The good news is that international buyers can get a mortgage in Portugal. The process is paperwork-heavy, especially if your income is paid outside Portugal, but it’s manageable when you prepare early and avoid making an offer before you know your borrowing position.

Answer first: Yes, non-residents can get a mortgage in Portugal, usually with a larger deposit than Portuguese residents. Many international buyers borrow around 60–70% of the bank’s valuation, though income, age, currency, property type and lender policy all matter. Start with an affordability check, then compare fixed, variable and mixed-rate offers before signing a purchase contract.

Contents

- Can non-residents get a mortgage in Portugal in 2026?

- How much can you borrow?

- What deposit do international buyers need?

- Fixed, variable or mixed rate: which mortgage type should you choose?

- What documents do you need?

- How to get a mortgage in Portugal step by step

- How long does the mortgage process take?

- Should you use a mortgage broker in Portugal?

- How to improve your chances of approval

- What should I do next?

- Summary

- Frequently asked questions about getting a mortgage in Portugal

- Sources

Can non-residents get a mortgage in Portugal in 2026?

Yes. Portuguese banks and specialist lenders do lend to non-resident buyers, including buyers from the UK, USA and other non-EU countries. Most applications are assessed individually, so two buyers with similar budgets can receive different offers depending on income source, age, existing debts and the property being bought.

The official lending framework in Portugal requires banks to assess your creditworthiness before approving a loan. That assessment can include your age, employment status, income, regular expenses, existing debts, credit records and the likely effect of interest-rate rises on your repayments. A positive assessment also doesn’t force the bank to lend – it simply means you’ve passed that stage of its risk review.

For non-resident buyers, the practical test is usually stricter than the headline mortgage rules suggest. If your income is in pounds or dollars, the bank may stress-test your application against exchange-rate movement. If you’re older, self-employed or buying a property that will not be your main residence, the lender may reduce the loan-to-value or shorten the repayment term.

For a detailed guide on the rest of the process, claim your free copy of our Portugal buying guide:

Free Portugal guide

Planning your Portugal purchase?

Your mortgage is only one part of the buying process. Our free Portugal Buying Guide walks you through the key steps, from deposits and legal checks to buying costs, timelines and completion.

- Buying process explained step by step

- Costs, taxes and legal checks covered

- Useful before viewing trips or making an offer

How much can you borrow?

As a guide, many non-resident buyers can expect to borrow around 60–70% of the property value. Some lenders may offer less, especially if your income is self-employed, paid in a foreign currency or less regular than a monthly salary or pension.

Portuguese lending limits are based on the lower of the purchase price and the bank’s valuation. This matters. If you agree to buy a property for €400,000 but the bank values it lower, your mortgage offer may be based on the bank’s valuation, not the price you agreed with the seller.

Banco de Portugal’s macroprudential rules set different loan-to-value limits depending on the purpose of the property. Loans for a borrower’s own permanent residence can generally go higher than loans for other purposes, while credit for properties that are not a main residence is capped lower. Debt-service-to-income should, as a rule, not exceed 50% of net monthly income, though banks can apply their own tighter standards.

| Buyer profile | Typical lending position | What it means in practice |

|---|---|---|

| Portuguese resident buying main home | Can often borrow more | Higher loan-to-value may be available if income and risk checks pass |

| Non-resident salaried buyer | Often around 60–70% | Stronger applications usually have stable income and clean debt records |

| Self-employed non-resident buyer | Often lower | Expect extra accounts, tax returns and income evidence |

| Buyer with foreign-currency income | May be stress-tested more heavily | Exchange-rate movement can reduce the amount offered |

| Older buyer | Term may be shorter | Age at the end of the mortgage can limit borrowing |

What deposit do international buyers need?

Most international buyers should plan for a 30–40% deposit, plus buying costs. If you’re relying on a Portuguese mortgage, your available cash needs to cover three things: your deposit, taxes and fees, and a buffer if the bank valuation comes in below the agreed purchase price.

The deposit is not the same as your full cash requirement. Property transfer tax, stamp duty, notary fees, registration fees, legal fees and bank charges are usually paid separately from the mortgage. For a fuller breakdown of buying costs, link this article to YOH’s guide to the costs of buying property in Portugal.

It’s worth building in a currency buffer too. A UK buyer agreeing a euro purchase price while holding funds in pounds can see their effective budget move before completion. This is where speaking to Smart Currency Exchange early can help you plan how and when to move money, rather than leaving the exchange rate to the final week.

Fixed, variable or mixed rate: which mortgage type should you choose?

Portuguese mortgages are usually offered on a fixed, variable or mixed-rate basis. Your best option depends on your risk tolerance, income stability, repayment plans and how long you expect to keep the property.

Banco de Portugal says home loans can have variable, fixed or mixed rates. A variable rate is usually made up of a reference rate, commonly Euribor, plus the lender’s spread. A fixed rate keeps the instalment the same during the fixed-rate period, while a mixed rate starts with a fixed period before moving to a variable rate later.

| Mortgage type | How it works | Why buyers choose it | Main risk |

|---|---|---|---|

| Fixed rate | Rate stays the same for the agreed fixed period | Predictable monthly payments | Initial rate may be higher than a variable offer |

| Variable rate | Rate moves with Euribor plus the bank’s spread | Can benefit if rates fall | Payments can rise if rates increase |

| Mixed rate | Fixed for an initial period, then variable | Balance between early certainty and later flexibility | Payment can change after the fixed period |

For a 2026 market reference, Statistics Portugal reported that the implicit interest rate across Portuguese housing loan agreements was 3.088% in March 2026, while contracts closed in the previous three months averaged 2.830%. Those are market indicators, not a guaranteed rate for international buyers.

Euribor is the key benchmark to understand if you’re considering a variable or mixed product. The European Money Markets Institute is the official source for Euribor rates, and most Portuguese lenders will explain which Euribor term applies to your mortgage offer.

What documents do you need?

You’ll need to prove who you are, where your money comes from and that you can afford the loan. Start gathering documents before a viewing trip, because overseas applications often take longer if translations or extra checks are needed.

Expect to provide:

- Passport or national identity document

- Portuguese tax number, known as a NIF

- Proof of address in your current country of residence

- Three to six months of bank statements

- Proof of income, such as payslips, pension statements, rental income or dividends

- Latest tax return or tax calculation

- Employer letter, accountant letter or company accounts, where relevant

- Details of existing mortgages, loans and credit cards

- Proof of savings and deposit funds

- Credit report from your home country, if requested

- Property details, reservation agreement or promissory contract once you have found a property

A NIF is usually one of the first things to organise. Portugal’s tax authority treats the NIF as part of taxpayer registration, and foreign residents and non-residents may need one for tax obligations, contracts, banking and other formal steps in Portugal.

If you’re self-employed, expect more scrutiny. Lenders may ask for two or three years of accounts, tax returns, business bank statements and an accountant’s confirmation of your income. Retired buyers may need pension statements, investment statements and evidence that income is secure enough to meet repayments.

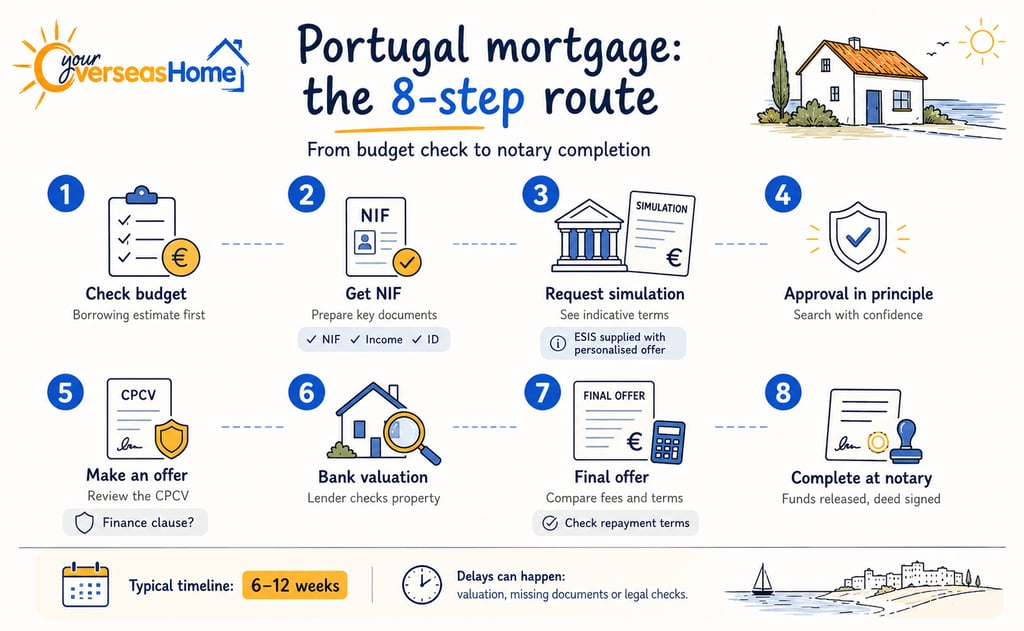

How to get a mortgage in Portugal step by step

1. Check your budget before viewing

Start with a borrowing estimate before you travel or make offers. This helps you decide which properties are genuinely affordable and whether your purchase depends on selling another asset, moving currency or reducing existing debts.

2. Get your NIF and prepare documents

Apply for your NIF, gather your income documents and check whether anything needs translating. If you’re using a lawyer, they can usually help you with the early administrative steps alongside the wider legal requirements for buying property in Portugal.

3. Request a mortgage simulation

The bank or broker will use your documents to produce an initial mortgage simulation. This gives you indicative terms, including the loan amount, rate type, monthly repayment and estimated costs.

When a lender approves a mortgage or provides a personalised simulation, it must provide a European Standardised Information Sheet. This document sets out the amount, term, interest rate, annual percentage rate of charge, fees, insurance requirements, repayment table and early repayment rules.

4. Get approval in principle

Approval in principle is not final approval, but it gives you a stronger basis for your property search. Estate agents and sellers will usually take you more seriously if you can show that your finance has already been assessed.

5. Make an offer and protect your position

Once your offer is accepted, your lawyer will review the documents before you sign the promissory contract, known as the Contrato de Promessa de Compra e Venda (CPCV). If your purchase depends on the mortgage, ask your lawyer whether the contract should include a finance condition.

6. Bank valuation and final approval

The lender appoints a valuer to assess the property. If the valuation supports the loan amount and your documents still pass the bank’s checks, the lender moves towards final approval.

7. Review the final offer

Read the mortgage offer carefully. Compare the spread, fees, annual percentage rate of charge, insurance conditions, early repayment terms and whether any lower rate depends on taking extra products.

For early repayment, Banco de Portugal says partial repayment can be made on an instalment date with advance notice, while full repayment also requires notice. Early repayment fees are capped at 0.5% of the repaid capital for variable-rate loans and 2% for fixed-rate loans.

8. Complete at the notary

At completion, the mortgage funds are released and the purchase deed is signed. Your lawyer and bank will coordinate the formalities, including registration of the mortgage against the property.

How long does the mortgage process take?

A straightforward application can take six to 12 weeks, but three months is a safer planning assumption if you’re applying from outside Portugal. The process can slow down if documents need translating, the bank asks for extra proof of income, the valuation is lower than expected or the property has legal issues.

| Stage | Typical timing | Main delay risk |

|---|---|---|

| Initial affordability check | A few days to two weeks | Missing income or debt information |

| Document preparation | One to three weeks | Translations, tax records or self-employed accounts |

| Mortgage simulation | A few days once documents are ready | Complex income structure |

| Approval in principle | One to three weeks | Bank requests extra evidence |

| Valuation and final offer | Two to six weeks | Valuation below agreed price |

| Completion | Depends on legal process | Contract, notary or registration delays |

Should you use a mortgage broker in Portugal?

You can apply directly to banks, but many international buyers use a broker because lender criteria vary. A good broker will know which banks are more open to non-resident income, self-employed buyers, pension income or applications from outside the EU.

Check that any credit intermediary is authorised. Banco de Portugal maintains lists of authorised credit intermediaries and entities authorised to act as intermediaries, so this is a basic due-diligence step before you share documents or pay a fee.

A broker can also help you compare the European Standardised Information Sheet across lenders. That matters because the lowest headline rate is not always the cheapest mortgage once fees, insurance and bundled products are included.

How to improve your chances of approval

Portuguese lenders want a clear, low-risk application. You can’t control every part of the bank’s decision, but you can make the file easier to approve.

Before applying:

- Reduce credit card balances and personal loans where possible

- Keep a clean paper trail for your deposit funds

- Avoid moving large sums between accounts without explanation

- Prepare tax returns, payslips and pension statements early

- Ask for a borrowing estimate before making offers

- Compare at least two mortgage offers

- Build a currency plan if your income or savings are not in euros

- Ask your lawyer how to protect your deposit if the mortgage is declined

It’s also worth reviewing your wider purchase plan. A mortgage is only one part of the transaction. You’ll still need legal support, tax planning, a property survey where appropriate and a safe way to transfer funds to Portugal.

For the wider buying process, link to YOH’s how to buy property in Portugal guide and the Portuguese property buying process article.

What should I do next?

If you’re hoping to buy with finance, start with the mortgage before the property. Speak to a Portugal mortgage specialist or regulated credit intermediary, confirm your likely loan-to-value and check how your age, income currency and deposit affect the offer.

Next, line up the practical support around the purchase: a lawyer, a currency plan and a realistic buying-cost estimate. Smart Currency Exchange can help you plan euro payments, while YOH can connect you with trusted Portugal specialists for the finance and legal steps.

Once you know your budget, use YOH’s where to buy property in Portugal guide to narrow your search, then compare areas such as the Algarve, Lisbon, Porto, Cascais and Madeira against your mortgage, tax and long-term ownership plans.

Summary

Non-residents can get a mortgage in Portugal, but they usually need a larger deposit than residents.

Many international buyers should plan around 60–70% borrowing, with a 30–40% deposit plus buying costs.

Portuguese lenders assess income, age, debts, property valuation and repayment risk before approving a loan.

Fixed, variable and mixed-rate mortgages are available, with variable products usually linked to Euribor.

Start the mortgage process before making an offer, especially if your income is in pounds or dollars.

Use a regulated broker or lender, compare the full cost of each offer and speak to a currency specialist early.

Frequently asked questions about getting a mortgage in Portugal

Yes. Portuguese banks offer mortgages to international buyers, typically financing up to 70% of the property’s value, depending on your income and nationality.

Documents usually include your passport, proof of income, bank statements, tax number (NIF), proof of address, and details about the property. All documents must be translated and notarised if not in Portuguese.

From initial assessment to funds being released, the mortgage process typically takes 6–12 weeks. Delays can occur if documents are missing or property valuations are lower than expected.

No, but it’s highly recommended. Brokers can match you with suitable banks, help negotiate better terms, and handle language and documentation issues.

Rates depend on the Euribor benchmark and your financial profile. In 2025, typical mortgage rates range from 3% to 5%, with better terms for those offering larger deposits or fixed-rate products.

Sources

- Banco de Portugal – creditworthiness assessment, LTV limits, maturity limits and debt-service guidance: https://clientebancario.bportugal.pt/en/creditworthiness-assessment

- Banco de Portugal – home loan pre-contractual information and European Standardised Information Sheet: https://clientebancario.bportugal.pt/en/how-enter-home-loan-agreements

- Banco de Portugal – fixed, variable and mixed-rate mortgage explanations: https://clientebancario.bportugal.pt/en/interest-rates-home-loans

- Banco de Portugal – early mortgage repayment rules and fee caps: https://clientebancario.bportugal.pt/en/how-repay-and-transfer

- Banco de Portugal – authorised credit intermediary register: https://clientebancario.bportugal.pt/en/authorised-credit-intermediaries

- European Money Markets Institute – official Euribor rate source: https://www.emmi-benchmarks.eu/benchmarks/euribor/rate/

- Statistics Portugal – March 2026 housing loan interest-rate release: https://www.ine.pt/xportal/xmain?DESTAQUESdest_boui=768022351&DESTAQUESmodo=2&xlang=en&xpgid=ine_destaques&xpid=INE

- Portal das Finanças – NIF and taxpayer registration information: https://info.portaldasfinancas.gov.pt/en/tax-information/getting-started-in-portugal/tax-identification-number/apply-for-your-nif/Pages/default.aspx