Moving to France is one of the most rewarding decisions you can make – but since the UK became a third country, the checklist list has grown. It’s no longer a case of packing a van and heading for the ferry. There are now strict windows for visa applications, healthcare registrations and customs declarations that all need careful sequencing.

In our experience, buyers who treat the relocation as a project – with clear milestones at the six, three and one-month marks – find the process far less stressful. This moving to France from the UK checklist is the modern roadmap for a successful move in 2026.

In short: A move to France from the UK in 2026 requires a long-stay visa (VLS-TS) applied for at least three months before travel, proof of income meeting the French minimum wage threshold and private health insurance. Pensioners should apply for an S1 form, and all movers need a customs inventory (Cerfa 10070) for duty-free removals.

Contents

T-minus 6 months: the planning phase

Six months out is the time to move from dreaming to doing. You need to establish which residency route you’ll take and make sure your finances are structured to meet French requirements.

Check your passport validity

Since Brexit, your passport must be less than 10 years old on the day you enter France and have at least 15 months of validity remaining to satisfy visa requirements. If yours is close to expiry, renew it now – a passport renewal currently takes up to 10 weeks through the UK Passport Office, and delays during your visa window could derail the timeline.

Audit your income and savings

To live in France without a local job, you’ll need to prove “sufficient means.” For 2026, consulates benchmark this against the French minimum wage (SMIC), which stands at €1,823 (£1,530) gross per month – roughly €1,400 (£1,175) net.

| Applicant type | Monthly income (approx.) | Annual equivalent |

|---|---|---|

| Single | €1,823 (£1,530) gross | €21,876 (£18,360) |

| Couple | ~€2,500 (£2,100) combined | ~€30,000 (£25,200) |

Many consulates prefer to see stable pension income. Significant savings (usually €30,000+ / £25,200+) can sometimes supplement a thinner monthly figure, but they’re rarely accepted as the sole proof.

Consult a currency specialist

Property prices and living costs are in euros, but your income will likely stay in pounds. Even a small shift in the exchange rate can move your purchasing power by thousands. Smart Currency Exchange can help you set up a forward contract to lock in a rate and protect your budget during the move – our guide to making essential payments in France explains how this works in practice.

Income thresholds at a glance (2026)

- Single applicant: €1,823 (£1,530) gross per month / €21,876 (£18,360) per year

- Couple: ~€2,500 (£2,100) combined per month / ~€30,000 (£25,200) per year

- Savings supplement: €30,000+ (£25,200+) may support a lower monthly figure but rarely accepted alone

- Source: Must be stable and documented – pensions, rental income or investment returns

- Proof required: Bank statements (6–12 months), pension letters or tax returns

T-minus 3 months: the visa and health window

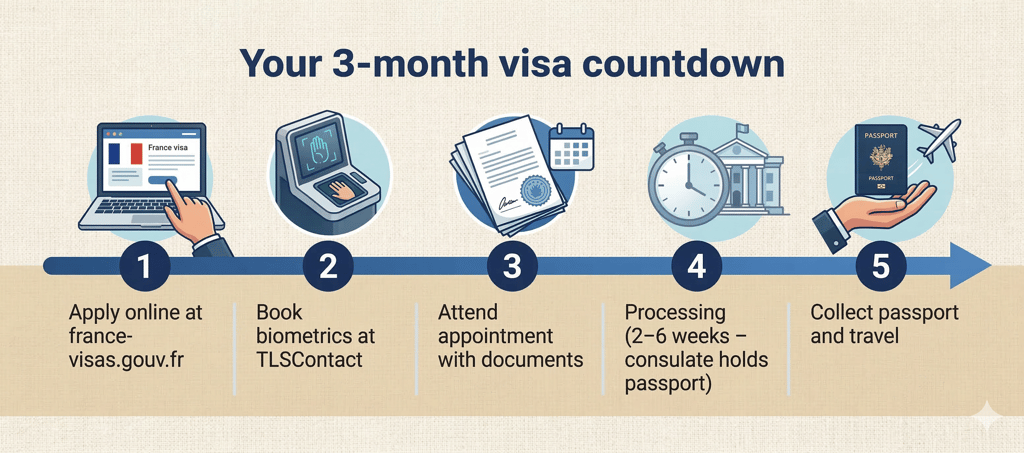

This is the critical action window. Most French consulates won’t accept visa applications earlier than three months before your planned departure date – and processing takes two to six weeks, so timing matters.

Apply for your VLS-TS Visiteur visa

Most UK retirees and lifestyle movers apply for the Visa de Long Séjour valant Titre de Séjour (VLS-TS) in the “Visiteur” category. It’s valid for 12 months and acts as your initial residence permit.

How to apply:

- Start your application at france-visas.gouv.fr

- Book a biometrics appointment at a TLScontact centre in London, Manchester or Edinburgh

- Attend your appointment with: proof of French accommodation (title deeds or a long-term lease), proof of income, private health insurance and a clean criminal record check (ACRO certificate)

- Allow two to six weeks for processing – the consulate will hold your passport during this time

Our guide to visa options in France for non-EU citizens covers all the available routes, including the Talent Passport for entrepreneurs and the specific requirements for remote workers.

Secure your health insurance

For the initial visa stamp, you’ll need private health insurance with at least €30,000 (£25,200) of cover and no deductibles or co-payments. This is non-negotiable – consulates reject applications without it.

If you’re a UK state pensioner, apply separately for your S1 form from the NHS Overseas Healthcare Services. The S1 entitles you to join the French state healthcare system (PUMA) on the same terms as French citizens, with the UK funding your care. It’s a significant benefit – but the private policy is usually still required alongside it for the visa application itself. Our guide to accessing French healthcare explains how PUMA, S1 forms and private cover work together.

Notify HMRC

Complete a P85 form to update your UK tax status. You’ll likely remain a UK tax resident until the end of the current tax year, but once you’re living in France for more than 183 days in a calendar year, you become French tax resident and must declare your worldwide income to the French authorities.

France and the UK have a double taxation agreement, so you won’t pay twice on the same income – but you will need to file a French tax return. Many buyers find it worth appointing a cross-border tax adviser for the first year.

T-minus 1 month: logistics and customs

With your visa in your passport, focus turns to the physical move. Customs rules for UK citizens have tightened, and the paperwork for your belongings is now as important as the belongings themselves.

Create your French customs inventory

To bring your household items into France without paying 20% VAT and 10% customs duty, you need to prove you’re relocating your primary residence.

What you’ll need:

- Cerfa form 10070 – the official customs declaration for personal property, completed in duplicate

- An itemised inventory in French listing estimated second-hand values in euros for every box and piece of furniture

- Proof of UK residence for 12+ months and proof of your French address

The six-month rule applies: only items you’ve owned and used for more than six months qualify for the exemption. Anything newer attracts full duty and VAT. Our detailed guide on what to bring from the UK to France covers the customs process, what’s worth shipping and what you’re better off buying locally.

Finalise removals and car plans

Decide whether you’re importing your UK car or buying in France. If importing, you’ll need a Certificate of Conformity from the manufacturer, a customs Certificate 846A and a French contrôle technique – your UK MOT is no longer accepted.

For the removal itself, use a firm experienced with post-Brexit “third country” customs clearance. This isn’t the time for an informal van hire – one missing document can hold your entire shipment at the French border. Our guide to moving your belongings to France covers how to choose a removal company and what to expect on moving day.

Month 1 in France: settling and compliance

Arrival is a milestone, but the administrative clock starts ticking the moment you cross the border. There are three tasks you can’t afford to delay.

Validate your VLS-TS online

You have three months to validate your visa through the official ANEF portal. This involves paying a digital tax stamp (timbre fiscal) of approximately €225 (£189) and uploading your passport, visa page and proof of French address. Miss this deadline and your visa becomes invalid – there’s no grace period.

Register with the CPAM

Once you’ve been in France for three months (or immediately if you hold an S1 form), apply to join the French healthcare system at your local Caisse Primaire d’Assurance Maladie (CPAM). This leads to your Carte Vitale – the green smart card that makes healthcare reimbursement automatic. The full registration process takes six to nine months, so start early. Our healthcare access guide walks through every step.

Exchange your driving licence

Under the 2022 Franco-British reciprocal agreement, UK driving licences issued after January 2021 must be exchanged for a French licence within 12 months of receiving your carte de séjour. No driving test is needed – it’s a direct exchange via the ANTS portal – but processing currently takes four to eight months, so apply as soon as you’re registered. Our transport in France guide covers driving rules, toll roads and licence requirements in detail.

First 90 days in France: your compliance checklist

☐ Validate your VLS-TS visa online via the ANEF portal (within 3 months – no grace period)

☐ Pay the timbre fiscal (~€225 / £189)

☐ Open a French bank account (needed for utilities, tax and healthcare)

☐ Register with CPAM for healthcare (or submit your S1 form immediately)

☐ Choose a médecin traitant (assigned GP) once your CPAM registration is underway

☐ Apply to exchange your UK driving licence via ANTS (allow 4–8 months processing)

☐ Obtain your numéro fiscal (tax number) from your local tax office

☐ Set up utilities – electricity, gas, water, internet

☐ Register at your local mairie if required by your commune

☐ Take out or confirm French home insurance (assurance habitation – mandatory for all residents)

Tick these off in order. The visa validation is the most time-sensitive – everything else flows from having legal residency confirmed.

Can you still buy property in France after Brexit?

In a word, yes. French property law – not EU law – governs ownership, and there are no restrictions on non-EU citizens buying property. The process hasn’t changed: you make an offer, sign a compromis de vente, allow 10 days for the cooling-off period and complete at the notaire’s office roughly three months later.

What has changed are the costs and the rules around spending time at your property. Frais de notaire on resale properties now run to approximately 7–9% following increases to the DMTO (departmental transfer tax) in most departments from April 2025. Non-EU residents selling property over €150,000 must appoint a fiscal representative. And social charges on capital gains are 17.2% for non-EU sellers, compared with 7.5% under the old EU-citizen rate.

If you’re buying as a second-home owner, you’re limited to 90 days in any 180-day period under Schengen rules – owning a property doesn’t extend this. For longer stays, you’ll need a visa.

Our guide to buying property in France covers the full process, while our costs guide breaks down every fee you’ll face.

What should I do next?

Your next step depends on where you are in the journey. If you’re still choosing a location, start with our region-by-region guide to France. If you’ve found a property and need to understand the buying process, our step-by-step guide to buying in France covers everything from offers to completion.

For help protecting your budget from exchange rate movements during the move, speak to a currency specialist at Smart Currency Exchange. And for a full picture of what daily life looks like once you’ve settled, explore our complete guide to living in France.

You can also browse property for sale in France to see what’s available in your chosen area right now.

Summary

Relocating to France in 2026 is a multi-stage project that rewards early planning. Start your passport and financial audit six months out to leave room for the three-month visa application window.

The VLS-TS Visiteur visa remains the most common route for retirees and lifestyle movers, requiring proof of income at or above the SMIC threshold (€1,823/month gross) and private health insurance.

Compliance doesn’t end at the border – validating your visa and registering for healthcare are your top priorities in the first 90 days.

With the right preparation, the move from the UK to your new French home can be smooth and stress-free.

Frequently asked questions

For a long-stay visa, you generally need to show a monthly income of at least €1,823 (£1,530) gross per person – equivalent to the French minimum wage. Beyond the visa, it’s worth having a settling-in fund of at least £10,000 to cover visa fees (~€325 total), removals and initial living costs while you wait for bank accounts and healthcare registrations to come through.

The Entry/Exit System (EES) is a biometric border check that became fully operational from April 2026. On your first entry, you’ll provide fingerprints and a facial scan. If you hold a valid VLS-TS visa or carte de séjour, you’re exempt from the 90-day Schengen tracking – but you’ll still go through the biometric registration.

Yes, but you’ll need to show the French consulate you have enough liquid funds to support yourself while waiting for the sale. You’ll also need proof of where you’ll live in France – a long-term rental contract works if your property purchase isn’t yet complete.

It’s not mandatory, but many buyers find a specialist relocation adviser invaluable for the VLS-TS application, particularly if income sources are complex (a mix of pensions, rental income and savings, for example). A bilingual notaire handles the property transaction itself.

Yes. There are no restrictions on non-EU citizens purchasing property in France. The buying process is unchanged, though costs have risen slightly (frais de notaire are now 7–9% on resale properties) and you’ll need a visa for stays longer than 90 days.